Cash buyers purchase lien properties because they offer guaranteed closings, discounted prices, and investment returns that financed buyers simply cannot access. A lien property, formally called an encumbered property, carries a legal claim against it from a creditor, tax authority, or government body. That complexity scares off most buyers. Cash buyers see it as an opening. Speed and certainty are the core motivations, and the data backs that up: cash buyers close in 10–14 days versus 30–45 days for financed deals. That gap is where real opportunity lives for investors and motivated sellers alike.

Why cash buyers purchase lien properties: the core advantages

Cash buyers hold a structural edge over financed buyers in every lien property transaction. The advantages are not subtle. They are decisive.

Speed is the most visible advantage. Cash closings take 10–14 days, while mortgage-backed purchases drag out 30–45 days or more. For a seller facing foreclosure or mounting tax debt, that difference is the gap between saving equity and losing everything.

No contingencies means no deal collapse. Financed buyers require appraisals and lender approval. Both can kill a deal at the last minute. Cash buyers skip both entirely. Sellers facing distressed situations, such as inherited properties with unpaid taxes or homes with judgment liens, prioritize guaranteed closings over squeezing out a higher price.

Commission savings add up fast. Sellers who accept a cash offer often avoid paying the standard 5–6% realtor commission. That savings alone can offset the discount a cash buyer negotiates. The math frequently favors accepting a lower cash offer over a higher financed one.

Here is a quick breakdown of what cash buyers bring to the table:

- No financing contingency, so the deal does not fall apart at the lender stage

- No appraisal requirement, removing a common deal-killer for distressed properties

- Faster closing timelines that protect sellers from additional interest or penalty accrual

- Ability to purchase properties in as-is condition without repair negotiations

Pro Tip: Many investors who call themselves "cash buyers" actually use short-term bridge loans or lines of credit to replicate the speed and certainty of a true cash offer. If you are competing in this space, that financing structure is worth understanding.

How do tax lien certificates create investment opportunities?

Tax lien investing is one of the most misunderstood strategies in real estate. The core mechanic is straightforward: when a property owner fails to pay property taxes, the local government sells a tax lien certificate at auction. The buyer pays the overdue taxes and earns interest until the owner redeems the debt.

Investors earn government-backed interest returns ranging from 8% to 36%, depending on the state. Redemption rates often exceed 95%, meaning most owners pay back the debt with interest. That makes tax lien certificates a reliable passive income vehicle, not a property acquisition play.

Here is how the process typically works:

- A county or municipality holds a public auction for delinquent tax liens.

- Investors bid on the certificates, often competing on interest rate or premium.

- The winning bidder pays the overdue taxes directly to the government.

- The property owner must repay the investor with statutory interest to clear the lien.

- If the owner fails to redeem within the statutory period, the investor may initiate foreclosure.

The distinction between tax lien and tax deed investing matters here. Tax lien investing targets the interest income. Tax deed investing means you are buying the actual property after foreclosure. Most experienced investors focus on the former.

| Investment Type | What You Buy | Primary Return | Foreclosure Risk |

|---|---|---|---|

| Tax Lien Certificate | Debt secured by property | 8%–36% annual interest | Low, most owners redeem |

| Tax Deed | Property after foreclosure | Equity and resale value | High, property condition unknown |

| Judgment Lien | Court-ordered debt claim | Negotiated settlement | Moderate, depends on equity |

Successful tax lien investors focus on steady passive income from high-interest redemption rather than foreclosure. Foreclosure is expensive, time-consuming, and legally complex. The real money is in the interest.

Why do cash buyers target lien properties at auctions?

Auctions are where cash buyers gain their sharpest competitive edge. The rules of most property auctions are designed in ways that eliminate financed buyers entirely.

Auction payment windows typically require certified funds within 24–48 hours. No mortgage lender in the country can underwrite and fund a loan in that window. Cash buyers, including those using hard money loans that close in 3–7 days, are the only realistic participants. That reduced competition directly translates to lower purchase prices.

Distressed sellers outside of auctions follow a similar logic. A homeowner facing foreclosure in New Jersey or a family managing an inherited property in Florida is not shopping for the highest bidder. They want certainty. They want the transaction done. Sellers in foreclosure or probate situations consistently accept lower cash offers because the alternative is a drawn-out process with no guaranteed outcome.

Off-market lien properties present another layer of opportunity. These are properties that never reach the MLS because the title complexity discourages traditional listing agents. Cash buyers who know how to navigate title searches, lien payoffs, and escrow coordination can access deals that most investors never see.

Pro Tip: Before bidding at a tax lien or distressed property auction, pull the property's full ownership history and check for municipal code violations separately from the standard title search. Auction properties often carry hidden liens that do not surface in a basic title report.

Here is how cash buyers compare to financed buyers in auction and distressed scenarios:

| Scenario | Cash Buyer | Financed Buyer |

|---|---|---|

| Auction payment deadline | Meets 24–48 hour window | Cannot close in time |

| Distressed seller negotiation | Offers certainty and speed | Offers uncertainty and delays |

| As-is property condition | Accepts without repair demands | Requires lender-mandated repairs |

| Title complexity | Navigates through escrow | Lender may decline to fund |

What risks should cash buyers weigh before purchasing?

Lien properties carry real risks. Understanding them is what separates profitable investors from costly mistakes.

The most dangerous pitfall is failing to identify municipal and code enforcement liens. These liens require separate searches from a standard title report. A city can place a lien for unpaid fines, demolition orders, or code violations, and that lien can carry higher repayment priority than a mortgage or judgment lien. Buyers who skip this step inherit the liability.

Here is what thorough due diligence looks like for lien properties:

- Order a full title search and a separate municipal records search for code violations

- Verify lien priority order: property taxes typically rank first, then municipal liens, then mortgages

- Confirm the property's physical condition before closing, since as-is purchases carry no warranty

- Coordinate with a title company to pay off all liens through escrow at closing

- Check the statutory redemption period if purchasing a tax lien certificate, since longer periods reduce your effective annual yield

Experienced buyers pay off liens at closing through escrow-coordinated payments. This protects the seller from needing cash upfront and protects the buyer by guaranteeing clear title transfer. The role of the title company in this process is not optional. It is the mechanism that makes the transaction legally clean.

One more risk worth flagging: the timing of tax lien redemption affects your actual return. Higher statutory rates with longer redemption periods can lower your effective annualized yield when capital is tied up for two or three years. A 36% statutory rate in a state with a three-year redemption window may underperform a 12% rate in a state where owners typically redeem within six months.

Key takeaways

Cash buyers purchase lien properties because speed, certainty, and reduced competition create opportunities for discounted acquisitions and reliable investment returns that financed buyers cannot replicate.

| Point | Details |

|---|---|

| Speed drives seller decisions | Cash buyers close in 10–14 days, giving distressed sellers certainty that financed buyers cannot match. |

| Tax liens offer passive income | Government-backed certificates yield 8%–36% interest, with redemption rates often above 95%. |

| Auctions favor cash buyers | Payment windows of 24–48 hours eliminate most financed competitors, reducing bidding pressure. |

| Municipal liens are a hidden risk | Code enforcement liens require separate searches and can carry higher priority than mortgages. |

| Escrow protects both parties | Title companies coordinate lien payoffs at closing, ensuring clear title without seller upfront costs. |

What i have learned about cash buyers and lien properties

Most people assume cash buyers target lien properties because they want to steal a deal. That framing misses the real picture. The investors I have seen succeed in this space are not predatory. They are disciplined. They understand that the value they offer, speed and certainty, is genuinely worth something to a seller who is out of options.

The biggest mistake I see new investors make is treating foreclosure as the goal in tax lien investing. It is not. The steady 8%–16% annual interest returns are the strategy. Foreclosure is a costly, time-consuming process that most experienced investors actively try to avoid. If you go into tax lien investing hoping to acquire properties cheaply through foreclosure, you will likely be disappointed and out of pocket.

The auction angle is genuinely underappreciated. Most retail investors never participate in county tax lien auctions because the process feels opaque. That opacity is the opportunity. Learning how a specific county runs its auctions, what the statutory interest rates are, and how to pull municipal records separately from title searches puts you in a category most competitors never reach.

One thing I advocate strongly: build a reputation as a reliable cash buyer in your target market. Sellers, estate attorneys, and real estate agents talk. If you close fast, handle lien complexity without drama, and treat sellers fairly, you get referrals. That pipeline of off-market lien properties is worth more than any single deal.

— Alek

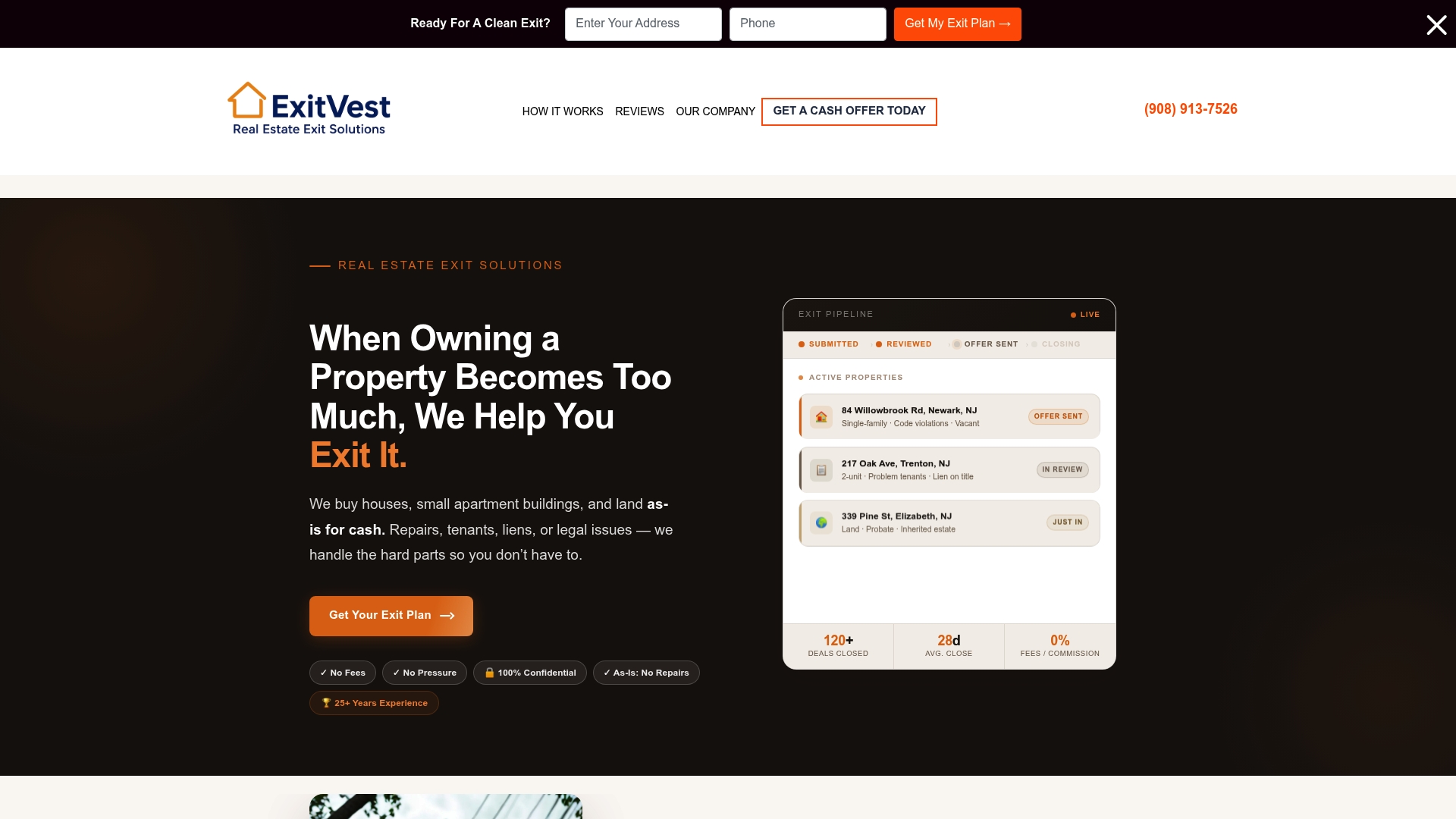

How Exitvest helps sellers move past lien complications

If you own a property with liens, unpaid taxes, code violations, or a title situation that feels too complicated to sell, Exitvest was built for exactly that scenario.

Exitvest makes fair cash offers on houses, land, and small apartment buildings across New Jersey, Texas, Florida, and Tennessee, and buys nationwide. There are no realtor commissions, no repair requirements, and no pressure to accept any offer. If your property has liens, Exitvest coordinates payoffs through escrow so you walk away clean. The process is straightforward: you describe your situation, receive a cash offer, and choose a closing timeline that works for you. See how it works or explore the full range of situations Exitvest handles to find out if your property qualifies.

FAQ

What makes lien properties attractive to cash buyers?

Lien properties attract cash buyers because title complexity and distressed seller circumstances reduce competition and create room for discounted acquisitions. Cash buyers can navigate lien payoffs through escrow in ways financed buyers and their lenders typically cannot.

How fast can a cash buyer close on a lien property?

Cash buyers typically close in 10–14 days, compared to 30–45 days for financed purchases. Hard money lenders can fund deals in as little as 3–7 days, which meets most auction payment deadlines.

Is tax lien investing the same as buying a foreclosed property?

No. Tax lien investing means purchasing a government-backed debt certificate and earning interest when the owner redeems it. Buying a foreclosed property means acquiring the actual real estate after the owner has lost it, which carries far more risk and complexity.

What is the biggest risk in purchasing a lien property?

The biggest risk is missing municipal or code enforcement liens, which require separate searches from a standard title report. These liens can carry higher repayment priority than a mortgage and leave the buyer responsible for unpaid city fines or violation penalties.

Do sellers benefit from accepting cash offers on lien-encumbered homes?

Yes. Sellers avoid the 5–6% realtor commission, eliminate the risk of deal collapse from financing or appraisal issues, and receive a guaranteed closing timeline. For sellers in foreclosure or probate, that certainty is often worth more than a higher financed offer.