Most people assume financing is the smart play in real estate. Borrow cheap money, put less down, and let leverage amplify your returns. That logic holds in many markets. But understanding why cash buyers purchase apartment buildings reveals a more nuanced picture, one where certainty, speed, and verified income often outperform the theoretical gains of leverage. In today's volatile rate environment, cash offers for apartment buildings are not just about convenience. They represent a deliberate strategic shift toward risk control, tax optimization, and negotiating power that financed buyers simply cannot match.

Table of Contents

- Key takeaways

- Why cash buyers purchase apartment buildings: the core financial advantages

- Market dynamics in 2026 pushing investors toward cash

- Real trade-offs cash buyers must accept

- Tax strategies that attract cash buyers to apartments

- Cash vs. financed apartment acquisitions: when each makes sense

- My perspective on cash buying in apartment buildings

- Sell your apartment building fast with Exitvest

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cash buyers save on price | Cash buyers often negotiate roughly 9% lower purchase prices by offering sellers speed and certainty. |

| Speed is a real competitive edge | Cash transactions can close in days or weeks, versus the typical 30 to 45 days for mortgage closings. |

| Tax benefits still apply | Depreciation and cost segregation give cash buyers significant after-tax advantages even without mortgage interest deductions. |

| Market conditions favor cash | High interest rates and supply constraints push investors toward stabilized, verified cash-flowing assets in 2026. |

| Risk control over return maximization | Cash buyers prioritize certainty and lower deal failure risk, especially for income-producing Class B apartment buildings. |

Why cash buyers purchase apartment buildings: the core financial advantages

The first reason is negotiation power. Sellers of apartment buildings are not just evaluating price. They are evaluating the probability that a deal will actually close. A financed buyer offering $2.8 million competes directly with a cash buyer offering $2.6 million, and the cash offer frequently wins. Cash buyers save about 9% on purchase price compared to financed buyers because sellers would rather take less money and sleep soundly than gamble on loan approval, appraisals, and underwriting timelines.

Speed is the second major driver. Cash transactions can close in days or weeks, while mortgage-backed closings average 30 to 45 days. For sellers facing distress, partnership disputes, or tax deadlines, that speed differential is worth real money. The benefits of cash buyers extend to sellers in ways that go beyond headline price, making cash offers structurally more attractive.

Here is what distinguishes cash transactions in apartment acquisitions specifically:

- No financing contingency. The deal does not collapse because a lender got cold feet after a rent roll review.

- No appraisal required. Cash buyers skip the third-party valuation step that frequently derails deals when lenders require a price reduction.

- Simplified due diligence. Without lender requirements, cash buyers control their own timeline and depth of inspection.

- Fewer closing costs. No origination fees, points, or lender title insurance means lower total acquisition cost.

Pro Tip: If you are a cash buyer, use your speed advantage explicitly in negotiations. Offer a shorter inspection period and a defined closing date. Sellers of apartment buildings value schedule certainty almost as much as price.

Market dynamics in 2026 pushing investors toward cash

Interest rate volatility has fundamentally changed the calculus for apartment building acquisitions. When debt was cheap, moderate leverage made mathematical sense. When rates are elevated and refinancing windows are uncertain, the cost of carrying floating-rate debt on a value-add project can turn a profitable business plan into a forced sale.

Higher-for-longer interest rates increase the cost of capital for risky deals and push investors toward assets with verified, current income. This means the investor appetite has rotated away from speculative repositioning plays and toward stabilized apartment buildings with clean rent rolls and audited operating histories.

Several converging forces define the 2026 market for cash buyers:

- Institutional mandates. Pension funds and REITs are required by charter to acquire stabilized income-producing assets. These buyers do not speculate on future rent growth. They buy current, verified yield.

- Supply constraints. New multifamily construction has slowed sharply due to higher construction loan costs. Existing inventory with proven occupancy carries a scarcity premium.

- Cap rate compression on quality assets. Stabilized Class B assets trade at 6.0 to 6.8% cap rates, while value-add properties trade at 7.2 to 8.0%, reflecting the premium the market assigns to certainty.

- Psychological shift. Post-pandemic volatility has made investors acutely aware of downside scenarios. Investor psychology now favors certainty and premium valuations for verified cash-flowing apartment buildings over optimistic projections.

These dynamics explain why investment in apartment buildings via cash has become a primary strategy for sophisticated buyers, not just a fallback when financing fails.

Real trade-offs cash buyers must accept

Honest analysis requires acknowledging what cash buyers give up. This is not a one-sided equation.

The most significant cost is opportunity cost. Capital deployed in an apartment building is illiquid. That same capital could fund multiple leveraged acquisitions, theoretically generating far higher aggregate returns. Cash buyers are making a deliberate trade: lower potential upside in exchange for lower risk and simpler execution.

The leverage math is real. If you purchase a $3 million apartment building outright and it appreciates 10%, you earn $300,000 on a $3 million deployment. A financed buyer who put $750,000 down on the same building earns the same $300,000 appreciation on only $750,000 of equity. That is a 40% return on equity versus a 10% return for the cash buyer. On paper, leverage wins when assets appreciate.

What cash buyers give up in leverage, however, they gain in risk profile. There is no debt service to cover during vacancy spikes. There is no lender covenant to trigger a loan acceleration. And there is no refinancing cliff to navigate in a tight credit market.

The tax side also shifts. Cash buyers lose the mortgage interest deduction, which can be substantial on a large loan. However, depreciation and cost segregation create offsetting paper losses that shelter other taxable income, keeping the after-tax return competitive.

Pro Tip: Before comparing cash vs. financed returns, model both scenarios on an after-tax, after-vacancy basis over a ten-year hold period. Most spreadsheets that favor leverage assume perfect occupancy and stable rates. Add realistic stress scenarios and the cash advantage becomes more visible.

Tax strategies that attract cash buyers to apartments

Many sophisticated investors do not buy apartment buildings primarily for current cash flow. They buy for the tax architecture.

Here is how the tax strategy works in practice:

- Depreciation deductions. The IRS allows residential rental properties to be depreciated over 27.5 years. On a $3 million building, that generates roughly $109,000 in annual depreciation deductions that reduce taxable income without any actual cash outflow.

- Cost segregation studies. A cost segregation analysis reclassifies components like flooring, fixtures, and HVAC systems into 5, 7, or 15-year schedules, accelerating those deductions into the early years of ownership. This can generate $200,000 to $400,000 in accelerated deductions in year one alone on a mid-sized property.

- Paper losses offsetting active income. Investors may buy apartment buildings with flat or even negative cash flow specifically because depreciation-driven paper losses offset other taxable income, creating real after-tax profitability.

- Long-term appreciation. Cash buyers with a ten-plus year horizon are willing to accept modest current yields because they believe the combination of tax shelter, debt-free equity growth, and eventual appreciation will outperform alternatives.

The profile of a cash buyer who leans on this approach tends to be a high-income professional, a business owner with substantial active income, or a fund with a mandate to acquire real assets that generate tax-efficient returns. For them, why invest in apartments is not about monthly cash flow statements. It is about total after-tax, after-appreciation wealth accumulation over a multi-decade hold. You can review how tax advantages influence strategy when evaluating multifamily acquisitions.

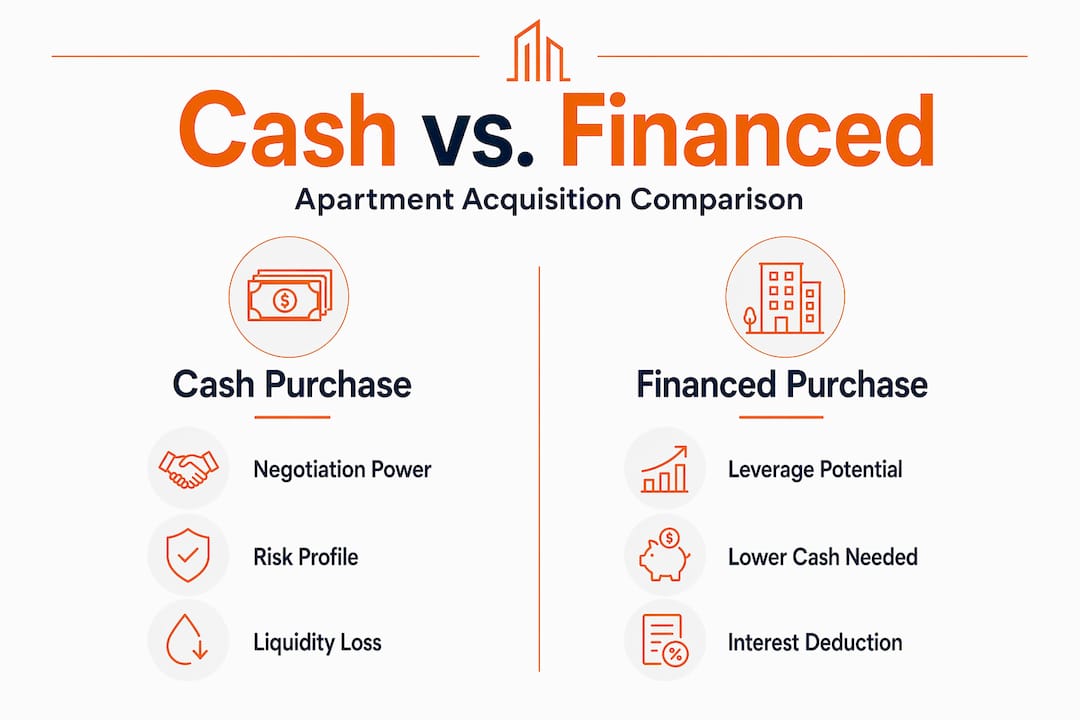

Cash vs. financed apartment acquisitions: when each makes sense

The honest answer is that neither strategy dominates universally. The right approach depends on interest rate conditions, the buyer's capital position, the asset's income stability, and the investor's risk tolerance.

| Factor | Cash purchase | Financed purchase |

|---|---|---|

| Negotiating position | Stronger. Sellers discount for certainty. | Weaker. Financing contingency adds risk. |

| Return on equity | Lower. No leverage amplification. | Higher in appreciation scenarios. |

| Closing timeline | Days to weeks. | 30 to 45 days, or longer. |

| Risk of deal failure | Minimal. | Moderate to high, depending on lender. |

| Debt service coverage | Not required. | Must maintain DSCR covenants. |

| Tax interest deduction | Not available. | Available and often substantial. |

| Capital efficiency | Low. Full capital deployed in one asset. | High. Capital spread across multiple assets. |

Cash buyers in real estate tend to favor this approach when they have limited appetite for execution risk, when the market is offering discounts for certainty, or when the tax efficiency of a debt-free hold outweighs the return enhancement of leverage. For a direct comparison of funding structures, understanding the rate and term environment is critical before committing.

Financed buyers win when rates are low, when the asset requires repositioning that creates forced appreciation, and when the investor has the operational capacity to manage a value-add execution plan. For investors exploring the Colorado multifamily market, local cap rate compression often makes leveraged acquisition the more competitive approach.

The shift in 2026 toward cash transactions reflects a market where the traditional financing edge has narrowed. Properties with verified NOI get a 15 to 20% premium price per door, which tells you exactly what buyers are paying for: audited, stable income that performs without the complexity of debt.

My perspective on cash buying in apartment buildings

I have watched this market long enough to know that the most dangerous deals are the ones that look brilliant on a spreadsheet with optimistic assumptions. Over-modeling rent growth leads to forced sales and negative leverage. I have seen that pattern repeat since 2021, and it is still playing out today.

What I find genuinely interesting about 2026 is how the definition of "smart money" has shifted. The cash buyers I watch are not avoiding leverage because they cannot access debt. They are avoiding it because verified income is now the most valuable commodity in the market, and they would rather own it outright than risk losing it to a lender covenant or a refinancing crisis.

My honest advice to analysts and investors weighing this decision: stop treating cash purchase as a conservative fallback. In the right market conditions, it is the aggressive play. You negotiate harder, close faster, and eliminate the single biggest reason apartment building deals collapse: financing failure. The certainty you bring to a seller has real monetary value, and most buyers never learn to price it correctly.

Simplicity is not a concession. Sometimes it is the edge.

— Alek

Sell your apartment building fast with Exitvest

If you own a small apartment building and want to exit quickly without the uncertainty of a traditional sale, Exitvest was built for exactly that situation.

Exitvest provides fair cash offers for apartment buildings nationwide, with a strong presence in New Jersey, Texas, Florida, and Tennessee. Whether you are dealing with problem tenants, deferred maintenance, financial pressure, or simply want to move on without months of uncertainty, the Exitvest process removes the friction. There are no agent commissions, no lender delays, and no appraisal surprises. You choose the closing timeline that works for your situation. Learn exactly how the process works and get a no-pressure offer today.

FAQ

Why do cash buyers pay less for apartment buildings?

Cash buyers often negotiate about 9% lower prices because sellers value the certainty and speed of a cash transaction over the higher but riskier financed offer. Removing financing contingencies reduces deal failure risk, which sellers price into their willingness to accept a lower number.

How fast can a cash transaction close on an apartment building?

Cash transactions can close in days or weeks, compared to the 30 to 45 days typical for financed purchases. This speed advantage comes from eliminating mortgage underwriting, appraisals, and lender approval steps.

Do cash buyers still get tax benefits without a mortgage?

Yes. While cash buyers lose the mortgage interest deduction, they still benefit from depreciation deductions and cost segregation strategies. Depreciation and cost segregation create paper losses that shelter taxable income and generate after-tax profitability even without positive cash flow.

Why are institutional investors buying apartment buildings with cash in 2026?

Institutional buyers like pension funds and REITs have mandates to acquire stabilized, income-producing assets. In a high-rate environment, verified cash flow is more valuable than speculative upside, and cash purchases remove the debt risk that makes value-add acquisitions dangerous.

What is the biggest trade-off for cash buyers of apartment buildings?

The primary cost is opportunity cost. Capital locked into a single apartment building cannot be deployed across multiple leveraged assets, which limits total portfolio returns in strong appreciation markets. Cash buyers accept lower potential upside in exchange for reduced risk, simpler execution, and stronger negotiating position.