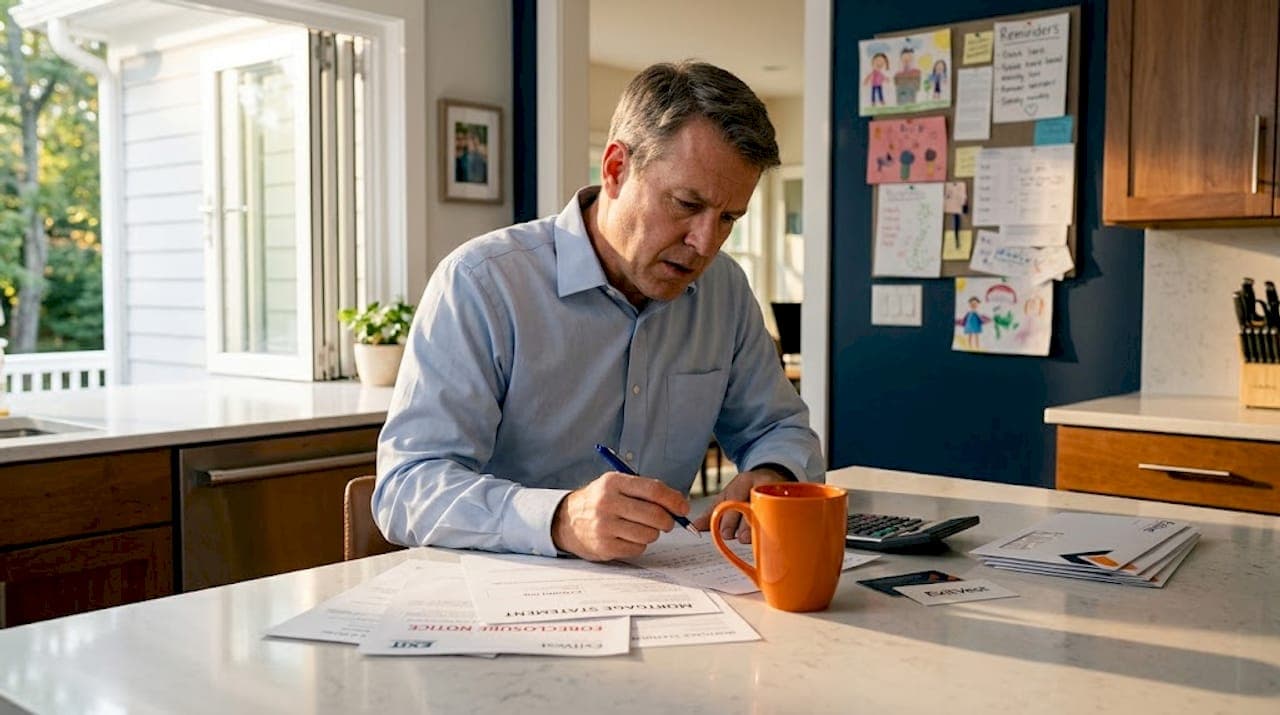

Facing foreclosure in New Jersey is one of the most stressful financial situations a homeowner can experience. The clock ticks toward a sheriff sale, your credit hangs in the balance, and the decisions you make in the next few weeks can shape your financial future for years. The good news: you have real selling home foreclosure New Jersey options available right now, and most homeowners still have more leverage than they realize. This guide breaks down every viable path, from cash sales to short sales to deed-in-lieu transfers, so you can act fast and protect what you've built.

Table of Contents

- Key takeaways

- Selling home foreclosure New Jersey options: what to know first

- 1. Selling to a cash buyer

- 2. Listing with a traditional real estate agent

- 3. Negotiating a short sale

- 4. Deed in lieu of foreclosure

- 5. Filing for bankruptcy

- 6. Loan modification as a parallel strategy

- 7. Protecting equity in property tax foreclosures

- Comparing your options side by side

- How to decide what is right for your situation

- My honest take on selling during foreclosure

- How Exitvest helps New Jersey homeowners sell fast

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Act before the sheriff sale | Selling before auction preserves equity and avoids a foreclosure record on your credit. |

| Cash buyers move fastest | Cash sales close in days or weeks, making them the strongest option when time is short. |

| Short sales take 60 to 120 days | Lender approval is required and takes time, so starting early is critical. |

| Bankruptcy can pause the process | Filing Chapter 13 triggers an automatic stay that halts the sheriff sale immediately. |

| Inherited and distressed homes qualify | As-is cash buyers purchase properties in any condition, including inherited or problem properties. |

Selling home foreclosure New Jersey options: what to know first

Before you pick a path, you need to size up your situation honestly. Not every option works for every homeowner, and choosing the wrong one wastes time you may not have.

Here are the key factors to evaluate before deciding:

- Time until sheriff sale. If you have 30 days or less, your options narrow fast. Cash sales and bankruptcy are the only realistic tools at that stage.

- Home equity. Most New Jersey homeowners still have equity when facing foreclosure. If your home is worth more than you owe, a traditional or cash sale likely makes sense.

- Property condition. Inherited homes, vacant properties, and distressed houses are harder to sell through a traditional agent. Cash buyers are built for exactly these situations.

- Your credit goals. A foreclosure record can damage your credit score for seven years. Selling before the sheriff sale, even at a discount, often protects your financial future better than waiting.

- Lender relationship. If you are behind on payments but still communicating with your lender, short sales and loan modifications may still be on the table.

- Deficiency exposure. In some cases, selling for less than you owe leaves a balance the lender can pursue. Understanding this before you sign anything is non-negotiable.

Pro Tip: New Jersey's Notice of Intent to Foreclose gives you a 30 to 180 day window before a formal complaint is filed. Use that time to gather documents, contact your lender, and explore your selling options, not just to worry.

1. Selling to a cash buyer

A cash sale is the fastest foreclosure exit available to New Jersey homeowners. Companies like Exitvest make offers on homes in any condition, skip the inspection and appraisal process, and can close in as little as seven to fourteen days.

The trade-off is price. Cash offers are typically lower than what you might get on the open market because the buyer absorbs renovation costs, carrying costs, and resale risk. But when the sheriff sale is weeks away, speed and certainty outweigh a higher number that may never materialize.

Cash sales work especially well for inherited homes, properties with deferred maintenance, and situations where the seller simply cannot afford to wait. There are no repairs, no showings, and no financing contingencies that can collapse a deal at the last minute.

2. Listing with a traditional real estate agent

If you have three to six months before your sheriff sale date and your home is in reasonable condition, a traditional listing can yield a higher sale price. A licensed agent markets your property to retail buyers, and competition can drive the price up.

The downside is time. The average New Jersey home sale takes 60 to 90 days from listing to closing, and that does not account for price negotiations, inspection repairs, or buyer financing delays. If your timeline is tight, a traditional listing is a gamble.

Pro Tip: If you pursue a traditional listing, ask your attorney about requesting a sheriff's sale adjournment. Adjournments can postpone the auction date and give you more time to complete a sale without the foreclosure going through.

3. Negotiating a short sale

A short sale happens when your lender agrees to accept less than the full mortgage balance as payment in full. It is a legitimate foreclosure exit that is less damaging to your credit than a completed foreclosure, but it requires lender cooperation and patience.

NJ short sales typically take 60 to 120 days to receive lender approval. That means you need to start the process well before your sheriff sale date. You will need to submit a hardship letter, financial statements, a comparative market analysis, and a purchase offer from a buyer.

The credit impact is real but manageable. Short sales are recorded as settled debt rather than foreclosure, which is meaningfully better for your long-term borrowing ability. One critical detail: negotiate a deficiency waiver in writing. Without it, your lender may pursue the remaining balance after the sale closes.

4. Deed in lieu of foreclosure

A deed in lieu is exactly what it sounds like. You voluntarily sign your property over to the lender in exchange for being released from your mortgage obligation. No sheriff sale, no auction, no public foreclosure record in the traditional sense.

This option works best when you have no equity, cannot sell the property fast enough, and want a clean exit. Lenders do not always accept deeds in lieu, particularly if there are other liens on the property. But when they do, it can be a dignified way to walk away without the full weight of foreclosure on your record.

5. Filing for bankruptcy

Bankruptcy is not a selling strategy. It is a delay strategy that buys you time to execute one of the options above. Filing Chapter 13 before the sheriff sale triggers an automatic stay, which immediately halts the foreclosure process.

Chapter 13 gives you a three to five year repayment plan to catch up on missed mortgage payments while keeping your home. Chapter 7 can also pause the process, but it does not provide a repayment structure, so the lender will eventually resume foreclosure.

Bankruptcy is a serious legal step with long-term credit consequences. Talk to a bankruptcy attorney before filing, and treat it as a tool to create breathing room, not as a permanent solution.

6. Loan modification as a parallel strategy

Selling is not always the only answer. If you want to stay in your home and have stable income, a loan modification can restructure your mortgage into something you can afford. New Jersey's judicial foreclosure process and mediation programs give homeowners more time than most states to submit complete applications.

Submitting a loan modification application during the Notice of Intent window triggers federal dual-tracking protections, which means the lender generally cannot push forward with foreclosure while a complete application is under review. This does not stop foreclosure permanently, but it creates a meaningful window to stabilize your situation.

7. Protecting equity in property tax foreclosures

If your foreclosure is driven by unpaid property taxes rather than a mortgage default, the rules are different and the stakes are higher. Property tax foreclosures can strip surplus equity from homeowners who do not take active legal steps to claim it.

If your home sells at a tax auction for more than you owe in taxes, you are entitled to that surplus. But you must file a sheriff's sale demand through New Jersey's JEDS system to preserve that right. Many homeowners lose this money simply because they did not know to ask. If you are facing a tax foreclosure, contact a housing attorney or a cash buyer immediately to explore your options before the auction date.

Comparing your options side by side

| Option | Speed to close | Credit impact | Price potential | Complexity |

|---|---|---|---|---|

| Cash buyer sale | 7 to 21 days | Minimal if before sheriff sale | Below market | Low |

| Traditional agent listing | 60 to 90+ days | Minimal if before sheriff sale | Market rate | Medium |

| Short sale | 90 to 150 days | Moderate (settled debt) | Below market | High |

| Deed in lieu | 30 to 60 days | Moderate | None (no proceeds) | Medium |

| Bankruptcy (Chapter 13) | Immediate pause | Significant | Depends on outcome | Very high |

| Loan modification | Varies | Minimal | N/A (you keep home) | Medium |

How to decide what is right for your situation

The best option depends on three things: how much time you have, how much equity you have, and what your financial life looks like after the sale.

Here is a practical decision framework:

- Less than 30 days to sheriff sale: Contact a cash buyer today and consider whether bankruptcy makes sense as a bridge. A no-obligation cash offer can be in your hands within 24 to 48 hours.

- 30 to 90 days remaining: A short sale or traditional listing may still be viable, but you need to move immediately. Start lender conversations and get a market valuation this week.

- Inherited or distressed property: Skip the traditional listing. Properties that need significant repairs or have title complications sell far more reliably to cash buyers who specialize in as-is purchases.

- Equity above your mortgage balance: Prioritize selling over short sales or deed in lieu. You have something to protect, and a sale, even a fast one, puts money in your pocket.

- No equity or underwater mortgage: Short sales and deed in lieu become your strongest credit-protecting options. Engage your lender early and document everything.

Pro Tip: Choosing between cash buyers and agents ultimately comes down to how much certainty you need versus how much time you can afford. If a higher price requires 90 more days and your sheriff sale is in 45, the math does not work in your favor.

My honest take on selling during foreclosure

I have seen homeowners in New Jersey sit on their options for weeks, convinced that something better will come along or that the lender will simply work it out. That denial is the most expensive mistake you can make. The foreclosure process has hard deadlines, and waiting costs you money, credit, and options.

The other thing I see constantly is homeowners undervaluing the certainty of a cash offer. A traditional listing at a higher price sounds better on paper. But when a buyer's financing falls through on day 60 and your sheriff sale is on day 75, that "better price" was never real. Certainty has real dollar value in a foreclosure situation.

If you have an inherited property or a home that needs serious work, do not waste weeks trying to list it traditionally. The buyers who can move fast and pay fairly for as-is properties are cash buyers, full stop. Get multiple offers, compare them honestly, and do not let pride about the number slow you down.

One more thing: document every conversation with your lender. Dates, names, what was said. Lender negotiations can stall or reverse without warning, and your paper trail is your protection if things go sideways.

— Alek

How Exitvest helps New Jersey homeowners sell fast

When time is short and the stakes are high, you need a buyer who can move quickly and handle complexity without drama. Exitvest works directly with New Jersey homeowners facing foreclosure, including those dealing with inherited properties, distressed homes, and situations where repairs are simply not possible.

The process is straightforward. You share your property details, Exitvest provides a no-obligation cash offer within 24 to 48 hours, and you choose your closing date. No repairs, no showings, no financing contingencies. If you need to stop foreclosure fast, Exitvest can close on your timeline, not a bank's. You can also learn exactly how the process works before committing to anything. There is no pressure and no obligation.

FAQ

Can I sell my home after foreclosure starts in New Jersey?

Yes. You can sell your home at any point before the sheriff sale takes place. Selling before the auction can protect your equity and prevent a foreclosure record from appearing on your credit report.

How long does a short sale take in New Jersey?

Short sales in New Jersey typically take 90 to 150 days from start to close, with lender approval alone taking 60 to 120 days. Starting the process as early as possible is critical.

What is the fastest way to sell a foreclosure property in NJ?

Selling to a cash buyer is the fastest foreclosure sale option in NJ. Cash buyers can close in as little as seven to fourteen days, require no repairs, and eliminate financing contingencies that slow traditional sales.

Does selling before sheriff sale protect my credit?

Yes. A completed foreclosure stays on your credit report for up to seven years. Selling your home before the sheriff sale, through any method, generally prevents that record from appearing and limits long-term credit damage.

Can I sell an inherited home in foreclosure in New Jersey?

Yes. Inherited homes in foreclosure can be sold, including to cash buyers who purchase properties as-is. If the property has title complications or deferred maintenance, a cash buyer is typically the most practical and fastest route.