Most homeowners assume that a cash sale is simpler than a traditional financed deal. No bank, no lender, no problem. But the role of title company in cash sale transactions is every bit as critical as it is when a mortgage is involved. Without a lender watching over the process, the responsibility for protecting your money and your legal ownership falls almost entirely on you and the title company you choose. This article breaks down exactly what title companies do in cash deals, why skipping their services is a serious mistake, and what you need to know before you sign anything.

Table of Contents

- Key Takeaways

- Role of title company in cash sale: the core duties

- Why title searches and insurance matter even more in cash deals

- How title companies manage escrow in cash transactions

- Misconceptions and legal nuances sellers should know

- My honest take on title companies in cash sales

- Sell your property with confidence through Exitvest

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Title search is non-negotiable | A title company uncovers liens, unpaid taxes, and ownership disputes before closing protects you from inheriting someone else's debt. |

| Owner's title insurance pays off long-term | A one-time premium at closing covers you indefinitely against defects that surface after the deal is done. |

| Escrow protects both parties | The title company holds your funds securely until every condition is satisfied, removing the risk of direct cash transfers. |

| Sellers still owe full disclosures | Title companies do not shield sellers from liability for property defects they failed to disclose to the buyer. |

| Cash deals move faster with title support | Title company involvement keeps the closing legal, clean, and free of costly surprises that can derail a quick sale. |

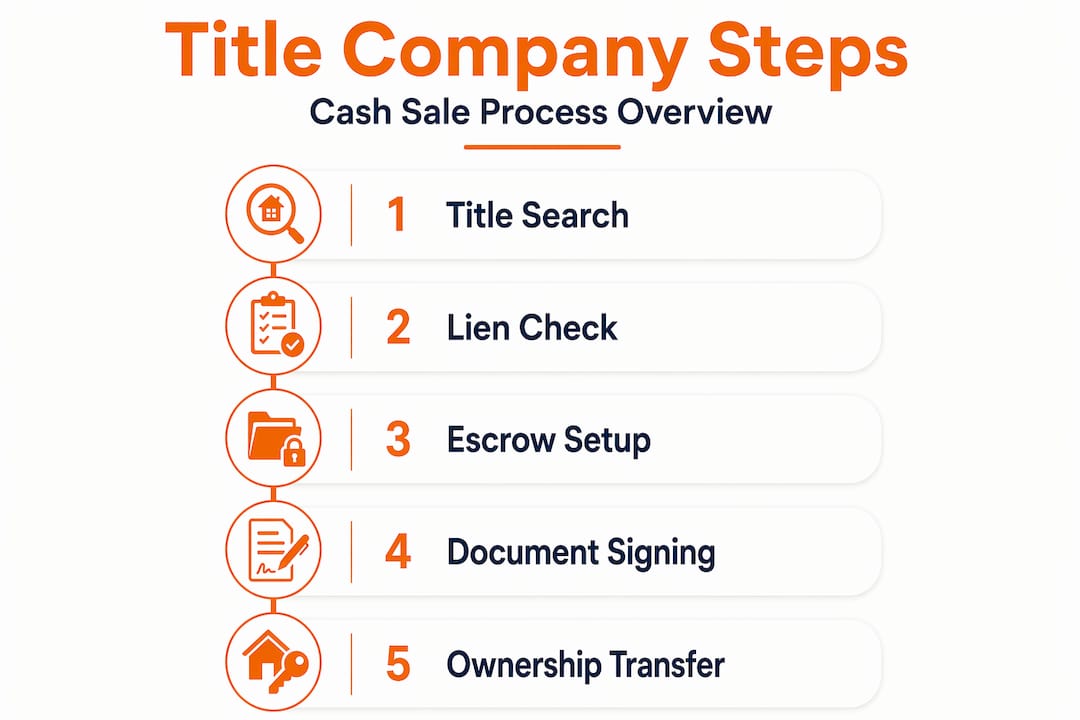

Role of title company in cash sale: the core duties

The most fundamental job of a title company is to confirm that the person selling a property actually has the legal right to sell it. This sounds obvious, but public property records are messier than most people realize. Previous owners, divorce proceedings, unpaid contractor invoices, and old tax bills can all create claims against a property that survive the sale and attach to the new owner.

Title companies conduct thorough searches to identify unpaid taxes, liens, or ownership claims before closing. In a financed deal, the lender demands this process because they have money at stake. In a cash deal, nobody is forcing anyone to do it. That makes your choice to hire a reputable title company your own personal financial defense.

Beyond the title search, here is what a title company handles during a cash sale:

- Title examination: Reviewing decades of public records to confirm a clean chain of ownership with no gaps or competing claims

- Title insurance issuance: Providing an owner's policy that protects you against defects that were not discoverable during the search

- Escrow management: Holding the buyer's funds in a neutral account until all closing conditions are satisfied

- Document preparation and coordination: Preparing the deed, settlement statement, and transfer documents required for legal ownership change

- Recording the deed: Filing the new deed with the county after closing so the transfer becomes part of the official public record

Title companies also pay off existing mortgages and liens with sale proceeds, then record the new ownership before releasing the remaining funds to the seller. The entire closing process runs through them.

Pro Tip: Ask your title company for a preliminary title report before you even finalize your sale agreement. Knowing about problems early gives you time to fix them without delaying closing.

Why title searches and insurance matter even more in cash deals

Here is the counter-intuitive truth about cash sales: they actually carry more risk for buyers than financed deals, not less. In a traditional mortgage transaction, the lender hires an appraiser, orders a title search, and requires title insurance on their own behalf. All of that due diligence happens whether the buyer requests it or not.

In a cash deal, none of that is automatic. Without lender-mandated insurance, the buyer assumes full risk. That means if a long-lost heir shows up two years after closing claiming co-ownership of the property, you are dealing with that lawsuit out of pocket unless you have an owner's title insurance policy in place.

The financial exposure is not theoretical. Skipping title searches risks assuming debts or liens that can surpass $50,000 after closing. Consider the scenarios that title insurance actually protects against:

- An unpaid contractor placed a mechanics lien on the property before the sale that was missed during a surface-level search

- A forged deed in the property's history creates a competing ownership claim decades later

- Boundary disputes or survey errors that affect the legal description of the land

- Probate issues from an estate sale where not all heirs properly signed off on the transfer

"Title insurance is a contractual indemnity that not only covers financial loss but legally defends against ownership challenges post-sale." Source

That legal defense aspect often surprises people. Title insurance policies include legal defense obligations, meaning the insurer steps in and fights the claim on your behalf. You do not pay attorney fees out of pocket while the dispute is resolved. And unlike homeowner's insurance, title insurance premiums are paid once at closing and the coverage lasts as long as you own the property. There is no annual renewal, no premium increase, and no expiration.

How title companies manage escrow in cash transactions

The word "escrow" sounds technical, but the concept is straightforward. When you agree to sell your home for cash, you do not want the buyer handing you a bag of money in a parking lot. And the buyer does not want to wire $300,000 directly to a stranger before they have confirmed the deed is clean and ready to transfer. The title company solves this problem.

Title companies act as impartial escrow agents holding the buyer's funds securely until deed delivery and all closing conditions are met. Here is how that process works from start to finish:

- The buyer wires their purchase funds to the title company's escrow account, not to the seller.

- The title company confirms receipt and verifies the funds clear before proceeding.

- The title company completes all final checks: title is clear, documents are signed, and any agreed conditions are satisfied.

- On closing day, the title company releases the deed to the buyer and disburses the proceeds to the seller after paying off any outstanding liens or taxes.

- The title company records the new deed with the county to complete the legal transfer.

This structure protects both parties simultaneously. Sellers know the money is real and available. Buyers know their money is protected until they actually own the property. No handshakes, no personal checks, no risk of the deal falling apart with funds missing.

Pro Tip: Confirm that your title company's escrow account is insured and that they carry errors and omissions insurance. This protects you if a clerical mistake at the title company affects your closing.

Real estate buyers and sellers working with reputable title firms also benefit from guidance on protecting ownership rights during complex transactions, especially when timing and fund release depend on multiple moving parts.

Misconceptions and legal nuances sellers should know

Many sellers walk into cash deals assuming the title company handles everything and they can sit back and collect. That is only partly true. The function of title company in real estate is to facilitate a legal transfer, not to cover for a seller who withheld information about the property.

Title companies cannot shield sellers from liability for undisclosed property defects. If you know the roof leaks, the basement floods every spring, or there is a structural issue in the foundation, you are legally obligated to disclose that in most states. The title company processes the paperwork, but the honesty of those disclosures is entirely your responsibility.

Here are a few other legal nuances worth understanding before you close:

- The title company works for the transaction, not exclusively for you. They are neutral by design, which means they will not advocate for your interests over the buyer's.

- If a defect is discovered after closing that you knew about and did not disclose, the buyer can sue you directly. The title insurance policy does not protect the seller in that scenario.

- Some states require attorneys to be present at closing regardless of whether a title company is involved. Always verify your state's requirements before you set a closing date.

"Cash sales speed transactions but do not remove the need for full property condition disclosures and legal transfer processes." Source

The importance of title services in cash transactions is clearest here. A title company makes the mechanics of the deal work. But legal and ethical responsibility for what you disclose about your property rests entirely with you as the seller. Those two things are separate, and confusing them is where many sellers get into trouble.

My honest take on title companies in cash sales

I have seen sellers try to cut corners on cash deals. They figure that since there is no bank involved, fewer professionals need to be paid, and the title company feels like an optional expense. I get the logic. It is wrong, but I understand it.

What I have learned from watching these transactions is that the deals that skip proper title work are not faster. They are just problems that have not surfaced yet. A cash buyer who waives title insurance to speed things along is essentially gambling their entire purchase price on the hope that no one ever challenges their ownership. That is not a smart trade.

In my experience, the sellers who move fastest are the ones who hire a good title company early and let them run the process. The title search happens quickly, the escrow is set up in days, and the closing date holds because there are no last-minute surprises. The sellers who try to save a few hundred dollars on title services often end up delaying their own closing by weeks.

Many homeowners underestimate title services in all-cash transactions and mistakenly forgo title insurance, increasing their vulnerability to legal claims after closing. That statistic does not surprise me. What surprises me is that the cost of an owner's title insurance policy is a rounding error compared to the value of the property it protects.

If you are a seller, the title company is not your adversary in the transaction. They are the one neutral party whose job is to make sure the deal closes cleanly and legally. Work with them, give them what they ask for promptly, and you will close faster than you expect.

— Alek

Sell your property with confidence through Exitvest

If you are ready to sell your home, land, or small apartment building for cash, Exitvest makes the process clear and straightforward from the first conversation. Every cash offer we make comes backed by a closing process that includes full title company support, including title search, escrow management, and title insurance coordination.

You will never be left wondering where your money is or whether the paperwork is in order. Whether you are dealing with an inherited property, facing foreclosure, or simply want to move on quickly, we handle the details. Learn how we close or get your cash offer today and see exactly what a clean, protected cash sale looks like when it is done right.

FAQ

What does a title company do in a cash sale?

A title company conducts a title search, manages escrow, issues title insurance, prepares closing documents, and records the new deed. These functions protect both the buyer and seller even when no lender is involved.

Is title insurance required in a cash sale?

Title insurance is typically not legally required in a cash sale since no lender mandates it. However, skipping it exposes the buyer to significant financial risk from hidden liens or ownership disputes that can exceed $50,000.

How long does it take a title company to close a cash deal?

Cash closings with a title company typically take between one and three weeks, depending on how quickly the title search is completed and whether any issues require resolution before the deed can transfer.

Can a title company protect the seller from liability?

No. A title company facilitates the legal transfer of ownership but cannot protect a seller from liability for undisclosed property defects. Sellers remain legally responsible for accurate disclosures regardless of how the sale is structured.

Who pays the title company in a cash sale?

Fees are typically split between buyer and seller, though the exact arrangement is negotiable. These costs include the title search fee, owner's title insurance premium, escrow fee, and deed recording charges.