A cash home buyer is an individual or company that purchases property by paying 100% of the sale price upfront, without a mortgage or any lender financing. No bank approval, no underwriting delays, no financing contingencies that can collapse a deal at the last minute. For homeowners facing foreclosure, inherited property, problem tenants, or simply a home they no longer want, understanding how cash buyers work is the difference between a fast, certain exit and months of uncertainty.

Cash buyers represent a distinct category in real estate. Unlike a traditional buyer who submits an offer contingent on loan approval, a cash buyer proves funds through bank statements or a letter of funds before the transaction moves forward. Sellers gain speed and certainty in exchange for a typically lower sale price. That trade-off is the core of every cash transaction, and knowing it upfront helps you make a smarter decision.

What is a cash home buyer and how do they differ from financed buyers?

A cash home buyer eliminates the single biggest source of deal failure in residential real estate: mortgage financing. When a financed buyer's lender pulls approval, the deal dies. When a cash buyer commits, the deal moves. That distinction matters enormously to sellers who cannot afford a failed closing.

Financed buyers must satisfy lender requirements including property appraisals, title reviews, and underwriting checks that can take six to eight weeks. Cash buyers skip the lender entirely. They still verify the property and confirm title, but they control their own timeline. Cash purchases remain elevated because of their unmatched security in volatile mortgage rate environments, which appeals directly to sellers who prioritize certainty over maximum price.

The proof-of-funds requirement is the practical dividing line. Any legitimate cash buyer will provide a recent bank statement, a certified funds letter, or a line-of-credit confirmation before you accept their offer. If a buyer claims to be paying cash but cannot produce documentation within 24 to 48 hours of your request, treat that as a red flag.

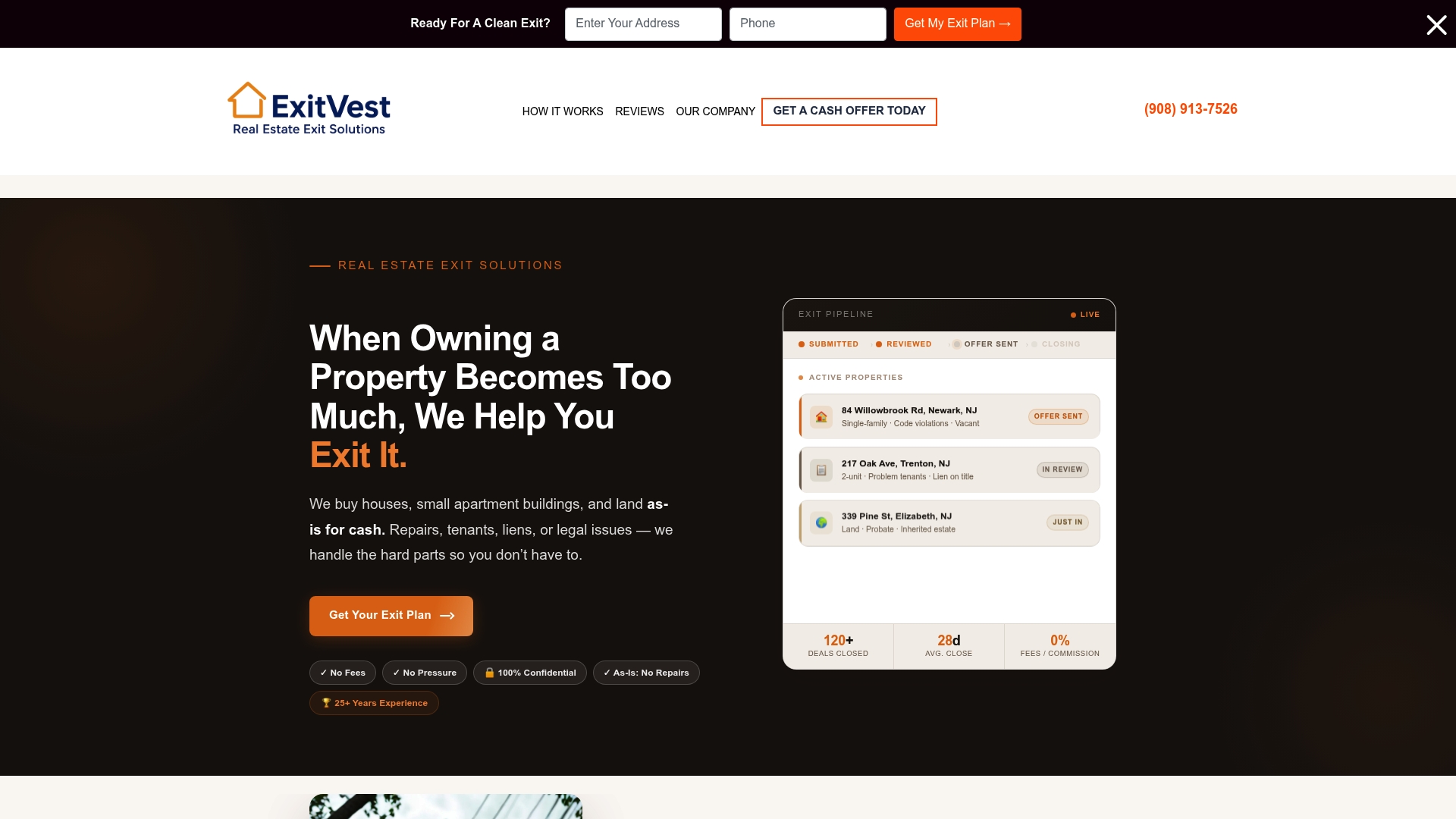

How the cash home buying process works from offer to closing

The cash home buying process follows a compressed version of a standard real estate transaction. Here is what you should expect at each stage.

-

Initial contact and property review. The buyer, whether an investor, a quick-sale company, or an individual, assesses your property. This may involve a brief walkthrough, photos, or a virtual tour. Many cash buyers will make a preliminary offer within 24 to 48 hours of reviewing the property.

-

Proof of funds and offer acceptance. Once you receive a written offer, request proof of funds immediately. After you verify the buyer's ability to close, you sign a purchase agreement. Unlike a traditional contract, this agreement typically contains no financing contingency.

-

Title search and due diligence. Cash buyers nearly always conduct title searches to uncover liens or legal issues before closing. This is a common misconception worth correcting: cash buyers do not skip due diligence. They simply skip the lender.

-

Closing. Cash sales typically close in 7 to 14 days, compared to the 45 to 60-day average for traditional financed sales. That is a four to six week difference that matters when you are facing a foreclosure deadline, a probate timeline, or a relocation date.

Pro Tip: Before signing any purchase agreement, confirm the closing date in writing and ask whether the buyer uses a licensed title company. A reputable cash buyer will have no hesitation providing both.

For a detailed breakdown of why this timeline gap exists, the cash closing timeline explained covers every stage where financed deals slow down and cash deals do not.

Benefits and trade-offs of selling to a cash home buyer

Selling to a cash buyer is not the right move for every homeowner. It is the right move for specific situations. Understanding both sides of the equation lets you decide with confidence.

The core benefits:

- Speed. A 7 to 14 day closing is not a marketing claim. It reflects the absence of lender timelines, appraisal scheduling, and underwriting queues.

- Certainty. Removing financing contingencies eliminates the most common reason deals fall apart. Sellers who have experienced a failed closing understand exactly what this is worth.

- As-is condition. Cash home buyers often purchase properties with repair or condition issues that would disqualify FHA and VA buyers. You do not need to repaint, replace appliances, or fix the roof before closing.

- Reduced costs. Sellers can avoid agent commissions averaging 6%, repair costs, and many closing fees. That savings partially offsets the lower sale price.

The primary trade-off:

Sellers accepting cash offers generally receive about 9% below market value on average. Cash buyers price in renovation costs, carrying costs, and transaction risk. That discount is the price of speed and certainty.

The situations where cash offers make the most sense include probate sales where heirs want a clean exit, pre-foreclosure where time is critical, landlords dealing with problem tenants, and owners of vacant homes accumulating costs. For a deeper look at why sellers willingly accept that discount, the reasons sellers accept lower offers article breaks down the math and the psychology behind the decision.

Who are cash home buyers? Types and motivations

Not all cash buyers are the same. Their motivations shape their offers, their timelines, and how they treat sellers throughout the process.

| Buyer type | Motivation | Typical offer | Process speed |

|---|---|---|---|

| Real estate investor | Rehab and resell or hold as rental | Below market, reflects repair costs | Fast, 7-14 days |

| Quick-sale company | Volume purchasing, as-is acquisitions | Standardized discount model | Very fast, often under 10 days |

| iBuyer (tech-enabled) | Algorithm-driven acquisitions | Closer to market, but with service fees | Moderate, 14-30 days |

| Individual cash buyer | Competitive offer, no financing needed | Near or at market value | Moderate, depends on buyer |

Cash buyers are often experienced investors who analyze properties in relation to current market conditions rather than simply targeting distressed sellers. That distinction matters because it means their offers reflect real calculations, not arbitrary lowballing. An investor offering 75% of market value on a property needing $40,000 in repairs may actually be offering fair value once you account for the work required.

Quick-sale companies, like Exitvest, specialize in as-is acquisitions with no pressure and no repair requirements. Individual cash buyers, often repeat homeowners using equity from a prior sale, tend to offer prices closer to market value but may not move as fast as professional buyers.

Pro Tip: When comparing offers from different cash buyer types, ask each one to show their proof of funds and their estimated closing date in the same conversation. The combination of both reveals who is actually ready to close and who is still figuring out their financing.

Practical considerations when selling your home to a cash buyer

Knowing how to evaluate a cash offer protects you from bad actors and helps you negotiate from a position of knowledge.

- Verify proof of funds before anything else. Ask for a bank statement dated within the last 30 days or a certified funds letter from a financial institution. Do not accept a verbal assurance or a screenshot that cannot be verified.

- Confirm the title process. Title searches in cash sales protect both parties. A buyer who resists using a licensed title company is a buyer worth walking away from.

- Negotiate the closing timeline. Cash buyers can close fast, but they can also accommodate your schedule. If you need 30 days to move, ask for it. Most professional cash buyers will agree to a flexible closing date.

- Understand the market context. In slower markets, cash buyers become more valuable. Memphis median days on market rose 26% year-over-year to 58 days in March 2026. When traditional buyers are scarce and listings sit, a cash offer gains leverage.

- Compare net proceeds, not just sale price. A cash offer of $240,000 with no agent commission and no repair costs may net you more than a $270,000 traditional sale after fees, staging, and repairs.

Pro Tip: Request a simple net proceeds worksheet from any cash buyer. Reputable buyers will provide one without hesitation. It shows the offer price minus any fees they charge, giving you a true apples-to-apples comparison with a traditional sale.

For sellers considering a quick sale without an agent, understanding these practical steps is what separates a confident decision from a regrettable one.

Key takeaways

A cash home buyer purchases property without mortgage financing, giving sellers a faster, more certain closing in exchange for a price that typically runs about 9% below traditional market value.

| Point | Details |

|---|---|

| Definition of cash buyer | A buyer who pays 100% of the purchase price upfront, with no lender or financing contingency. |

| Closing speed advantage | Cash sales close in 7 to 14 days versus 45 to 60 days for financed transactions. |

| Price trade-off | Cash offers average about 9% below market value, offset by savings on commissions and repairs. |

| Due diligence still applies | Cash buyers conduct title searches and may request inspections. They skip the lender, not the process. |

| Best-fit situations | Probate, foreclosure, vacant homes, problem tenants, and properties needing significant repairs. |

Why the conventional wisdom on cash buyers misses the point

Most articles about cash home buyers frame the conversation around price. Sellers are told to expect a discount and warned to be cautious. That framing is accurate but incomplete, and it causes sellers to make decisions based on the wrong variable.

The real question is not "how much will I lose?" It is "what is certainty worth to me right now?" I have seen sellers walk away from cash offers to chase a higher list price, only to sit on the market for four months, reduce the price twice, and ultimately net less than the original cash offer after carrying costs and agent fees. The math on speed is underestimated almost universally.

The 2026 market is making this clearer. Rising days on market in cities across New Jersey, Tennessee, and Texas mean that the traditional route carries real cost. Every month a property sits is a mortgage payment, a tax bill, an insurance premium, and a maintenance expense. Cash buyers are not just offering speed. They are offering the elimination of those ongoing costs.

The other misconception I encounter constantly is that cash buyers skip due diligence. They do not. A professional cash buyer will run a title search, review the property condition, and confirm there are no legal encumbrances before closing. The difference is that they do it on their own timeline, not a lender's.

My honest advice: if you are in a situation where time, certainty, or condition is a constraint, a cash offer deserves serious consideration. Run the net proceeds comparison. Factor in carrying costs. Then decide.

— Alek

Sell your home as-is with Exitvest

Exitvest buys houses, land, and small apartment buildings directly for cash, with no repairs required, no agent commissions, and no pressure to accept any offer. Whether you are dealing with foreclosure, an inherited property, a vacant home, or a situation you simply need to move past, Exitvest provides a straightforward cash offer based on your property's actual condition and your timeline.

The process is simple: submit your property details, receive a fair cash offer, and choose a closing date that works for you. Exitvest operates nationwide with a strong focus on New Jersey, Texas, Florida, and Tennessee. If you want to understand how the process works before committing to anything, that information is available with no obligation. For New Jersey homeowners specifically, the NJ cash for house page covers regional details and timelines.

FAQ

What does it mean when a buyer pays cash for a house?

A cash buyer pays the full purchase price from their own funds without taking out a mortgage. This eliminates lender requirements, financing contingencies, and the delays associated with underwriting and appraisals.

How fast can a cash home sale actually close?

Cash sales typically close in 7 to 14 days, compared to 45 to 60 days for traditional financed transactions. The exact timeline depends on the title search and any agreed-upon seller flexibility.

Do cash buyers still do inspections and title searches?

Yes. Cash buyers nearly always conduct title searches to identify liens or legal issues, and many request property inspections. Their advantage is the absence of a lender, not the absence of due diligence.

Will I always get less money selling to a cash buyer?

Cash offers average about 9% below traditional market value. However, sellers avoid agent commissions averaging 6%, repair costs, and many closing fees, which narrows the actual difference in net proceeds significantly.

When does a cash offer make the most sense?

Cash offers are most advantageous when speed or certainty is a priority, such as in foreclosure situations, probate sales, properties needing major repairs, or markets where homes are sitting for 45 or more days without offers.