You listed your home expecting top dollar, and then a cash buyer comes in 10% below asking price. Your first instinct is to say no. But here is what many sellers in tight situations discover too late: why sellers accept lower cash offers often has nothing to do with desperation and everything to do with math. When you factor in commissions, repairs, carrying costs, and the real risk of a financed deal falling apart, that lower number on paper can translate into more money in your pocket and far less stress along the way.

Table of Contents

- Key takeaways

- Why sellers accept lower cash offers: the core advantages

- The real math: why a lower offer can mean more money

- When urgent situations make cash the only logical choice

- Risks to watch for before you sign

- My take on when accepting less is actually winning

- How Exitvest helps you sell with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Speed has dollar value | Closing in 7 to 14 days eliminates mortgage, tax, and utility costs that eat into your proceeds. |

| Net proceeds tell the real story | A lower cash offer often beats a higher financed offer once commissions and repair costs are subtracted. |

| Certainty reduces risk | Cash deals skip financing and appraisal contingencies, so the sale is far less likely to collapse. |

| Urgent sellers gain the most | Foreclosure, probate, divorce, and relocation situations make timing worth more than list price. |

| Not all cash buyers are equal | Always verify proof of funds before signing anything to avoid wholesalers who cannot close. |

Why sellers accept lower cash offers: the core advantages

The benefits of cash offers in real estate go well beyond just getting paid faster. They change the entire structure of the transaction in ways that directly protect your bottom line.

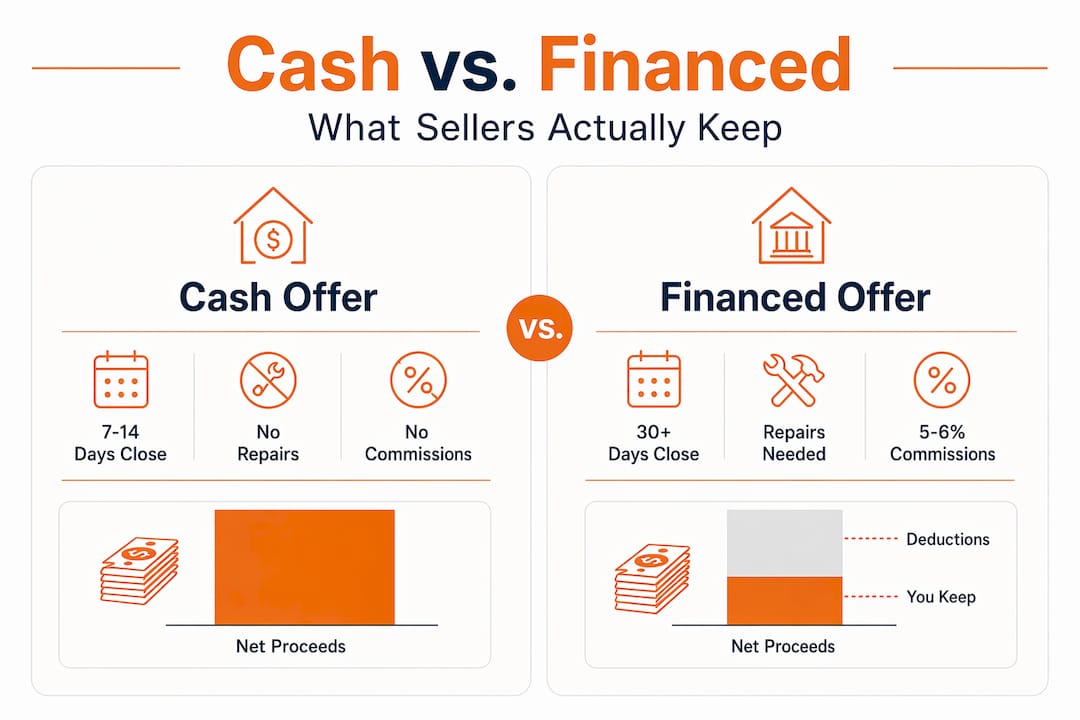

Speed is the most obvious benefit, but sellers routinely underestimate its financial weight. Cash transactions close in 7 to 14 days, compared to 30 to 45 or more days for financed sales. Every extra week on the market costs you real money in mortgage payments, property taxes, utilities, and insurance. Those costs are not hypothetical. They are monthly bills that keep arriving whether your home sells or not.

Beyond speed, cash offers deliver something financed deals simply cannot guarantee: certainty. Cash offers eliminate financing contingencies and appraisal requirements, which are two of the most common reasons deals fall through. When a buyer needs a mortgage, the lender controls the outcome as much as the buyer does. An appraisal that comes in low, a job change, or a dip in the buyer's credit score can kill a deal weeks after you thought it was done.

Here is what else sellers gain when they choose cash buyers:

- No repair requirements. Most cash buyers purchase properties as-is. You skip the contractor bids, the weekend projects, and the negotiations over what gets fixed before closing.

- Fewer contingencies. Cash deals typically involve fewer conditions attached to the sale, which means fewer opportunities for the buyer to back out.

- Less paperwork and fewer parties. No lender means no loan officer, no underwriter, and no bank-mandated inspections creating delays.

- Flexible closing timelines. Many cash buyers can work around your schedule, whether you need to close in a week or need 60 days to move out.

- Reduced emotional toll. Showings, open houses, and waiting for financing approval create weeks of uncertainty. Cash sales remove most of that stress.

Pro Tip: Before comparing any two offers, calculate your holding costs for each additional month the property stays unsold. Multiply your monthly mortgage, taxes, utilities, and insurance together. That number is what you lose for every 30 days a financed deal takes longer to close.

The real math: why a lower offer can mean more money

This is where most sellers have their mindset shifted. The headline offer price is not the same as what you actually take home. Lower cash offers can result in higher net proceeds than higher financed offers once you account for all the costs involved in a traditional sale.

Agent commissions average 5 to 6% of the sale price, and that comes directly off the top. Add repair costs, staging expenses, buyer concessions, and closing cost contributions, and the gap between a financed offer and a cash offer narrows fast. Sometimes it disappears entirely.

Look at this side-by-side comparison for a home with a $300,000 market value:

| Cost category | Financed offer ($310,000) | Cash offer ($280,000) |

|---|---|---|

| Agent commissions (5.5%) | $17,050 | $0 |

| Repairs and staging | $8,000 | $0 |

| Carrying costs (2 extra months) | $3,200 | $0 |

| Closing cost concessions | $4,000 | $0 |

| Estimated net proceeds | $277,750 | $280,000 |

The financed offer is $30,000 higher on paper. The cash offer actually puts more money in your hands. This is not a rare edge case. A cash offer is competitive when it nets within 5 to 12% below estimated listing proceeds after factoring in avoided costs. That is a wide range that covers most realistic scenarios.

Speed has measurable dollar value because holding costs accumulate every month a property sits unsold. Sellers often underestimate this. A two-month delay on a financed deal can easily cost $3,000 to $5,000 depending on your mortgage and local tax rates. That is money you will never recover.

Pro Tip: Run your own net proceeds calculation before rejecting any cash offer. Take the cash offer amount and subtract nothing. Then take the financed offer, subtract agent commissions, estimated repairs, expected carrying costs, and any concessions. Compare the two final numbers, not the headline prices.

When urgent situations make cash the only logical choice

The reasons for accepting cash offers shift significantly when your circumstances involve time pressure or property complications. For sellers in these situations, the lower cash offers advantages are not just financial. They are practical and sometimes the only realistic path forward.

Sellers facing foreclosure, probate, divorce, or urgent relocation place enormous value on speed and certainty. A traditional listing that takes three months to close does not help someone who needs to stop a foreclosure filing next week. It does not help an executor trying to settle an estate across state lines, or a couple in a contentious divorce who need to divide assets and move on.

Here are the seller profiles who most consistently benefit from accepting lower cash offers:

- Homeowners facing foreclosure. Time is the asset. Selling quickly to a cash buyer can stop the foreclosure process, protect your credit, and put money in your pocket rather than losing the home entirely. If this is your situation, stopping foreclosure fast is worth far more than holding out for a higher offer.

- Heirs managing inherited property. Probate properties often come with deferred maintenance, unclear title issues, or family disagreements. Cash buyers buy as-is and handle complexity without requiring the estate to fund repairs first.

- Landlords with problem tenants. Selling a tenant-occupied property through traditional channels is difficult. Most retail buyers want vacant homes. Cash investors buy occupied properties and deal with the tenant situation themselves.

- Sellers relocating on a deadline. A job transfer that starts in three weeks does not allow time for a 45-day financed closing. Cash buyers align with your timeline, not a lender's schedule.

- Owners of properties with significant damage or code issues. Homes with structural problems, fire damage, or unpermitted work rarely qualify for conventional financing. Cash is often the only viable option.

- Sellers who simply want out. Sometimes a property has become a financial or emotional burden. The lower cash offers advantage here is freedom. You close, you move on, and you stop paying for something you no longer want.

Risks to watch for before you sign

Knowing why sellers accept lower cash offers is only half the picture. You also need to know how to protect yourself in the process. Not every buyer waving a "cash offer" sign is actually ready to close.

- Wholesalers are not buyers. Some wholesalers use accepted contracts without having funds and then try to sell the contract to a real buyer before closing. Wholesalers typically offer 60 to 65% of after-repair value and often cannot close themselves, leading to last-minute renegotiations or cancellations that waste weeks of your time.

- Always request proof of funds. A legitimate cash buyer can produce a bank statement or letter from a financial institution confirming available funds. If a buyer hesitates or offers vague assurances, that is a warning sign.

- Watch for last-minute price reductions. Some buyers make a strong initial offer and then reduce it after the inspection period, betting that you are too committed to the timeline to walk away. Know your floor price before you start negotiating.

- Understand who you are dealing with. Not all cash offers are equal. An owner-occupant paying cash is very different from a wholesaler. Some owner-occupants pay significantly more than investors because they plan to live in the home and can absorb renovation costs themselves.

- Read the contract carefully. Even in cash deals, inspection contingencies and due diligence periods can give buyers room to exit. Know what you are agreeing to before you sign.

My take on when accepting less is actually winning

I have worked with enough sellers to say this plainly: the ones who regret accepting a cash offer are almost always the ones who did not run the numbers first. The ones who regret not accepting a cash offer are the ones who watched a financed deal collapse after 60 days, then had to relist, reprice, and start over.

What I have learned is that sellers in urgent situations tend to already understand the value of certainty. They are not naive. They are making a calculated trade. What trips people up is the emotional weight of seeing a lower number and feeling like they are giving something away.

The truth is that the impact of cash offers on negotiations is not just about price. It is about risk transfer. When you accept a cash offer, you are eliminating the buyer's ability to use a lender's timeline, appraisal, or financing denial as leverage against you. That is worth something real.

My advice: do not evaluate any offer in isolation. Evaluate it against your actual alternatives, your actual timeline, and your actual costs. A $280,000 cash offer that closes in ten days is not the same as a $310,000 financed offer that might close in 45 days or might not close at all. Selling your property as-is removes layers of uncertainty that most sellers do not fully account for until they have lived through a failed deal.

— Alek

How Exitvest helps you sell with confidence

If you are weighing a cash offer right now, or wondering whether your situation qualifies, Exitvest makes the process straightforward. We buy houses, land, and small apartment buildings nationwide, with deep experience in New Jersey, Texas, Florida, and Tennessee. We work specifically with sellers facing foreclosure, inherited properties, problem tenants, needed repairs, or financial pressure.

When you work with Exitvest, you get a transparent cash offer with no agent commissions, no repair requirements, and a closing timeline that fits your situation. We verify our own funds and never tie up your property with a contract we cannot close. You can get a cash offer today and compare it against your traditional sale estimate with full clarity. If you want to understand how our buying process works before making any decisions, that information is available with no pressure and no obligation. We are here when you are ready.

FAQ

Why do sellers accept lower cash offers instead of waiting?

Sellers accept lower cash offers because the net proceeds often match or exceed what a financed offer would deliver after subtracting commissions, repairs, and carrying costs. Speed and certainty also have real financial value that a higher headline price does not always offset.

How much lower can a cash offer be and still make sense?

A cash offer is generally competitive when it falls within 5 to 12% below your estimated net proceeds from a traditional listing. Beyond that range, the math typically favors waiting for a financed buyer unless your situation involves urgent timing.

What are the biggest risks of accepting a cash offer?

The main risks include wholesalers who cannot actually close, last-minute price reductions after the inspection period, and buyers who lack verified funds. Always request written proof of funds and understand the contract terms before committing.

Do cash buyers always buy homes as-is?

Most cash buyers, particularly investors, purchase properties as-is without requiring repairs or staging. This is one of the core benefits of cash offers in real estate for sellers dealing with deferred maintenance or property damage.

How fast can a cash sale actually close?

Cash transactions typically close in 7 to 14 days, compared to 30 to 45 or more days for financed sales. The exact timeline depends on the buyer's process and any title or legal issues that need to be resolved first.