If you're facing foreclosure, mounting debt, or a property you simply can't afford to fix, selling home without repairs explained correctly could be the financial lifeline you need. Most homeowners in distress assume they have to choose between spending thousands on repairs or accepting an embarrassingly low offer. That's not actually true. Selling as-is, which is the recognized industry term for a no repair home sale, gives you a legal and practical path to close quickly, protect your equity, and move on without pouring money into a property you're ready to leave behind.

Table of Contents

- Key Takeaways

- Selling home without repairs explained: what it really means

- Repair vs. equity: when skipping repairs actually makes financial sense

- How to prepare and market your home when selling without fixing

- Navigating inspection contingencies and buyer negotiations

- Lead paint rules and lender repair requirements you cannot ignore

- My honest take on selling as-is during financial distress

- How Exitvest makes selling as-is simpler

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| As-is sales still require disclosure | You must reveal known defects in writing; the as-is clause only eliminates your repair obligation. |

| Skipping repairs can protect equity | When repair costs exceed what they add in market value, selling without fixing often nets you more money. |

| Cash buyers are your best option | Investors and cash buyers skip lender requirements, closing faster without demanding repairs first. |

| Inspection rights belong to the buyer | Even in as-is deals, buyers can inspect and negotiate, though you are not obligated to fix anything. |

| Lead paint rules apply to pre-1978 homes | Federal disclosure law requires an EPA pamphlet and disclosure of known hazards before any sale. |

Selling home without repairs explained: what it really means

The term "as-is sale" has a specific legal meaning most people get wrong. An as-is clause means you will not make repairs or offer repair credits, but it does not strip buyers of their right to inspect the property and negotiate based on what they find. That distinction matters enormously.

Here is what the as-is framework actually covers:

- No repair obligation: You are not required to fix anything, regardless of inspection findings.

- No repair credits: You will not reduce the price or offer closing cost help specifically tied to repair issues unless you choose to.

- Full buyer inspection rights: Buyers can still hire inspectors, request records, and walk away if the condition is unacceptable to them.

- Disclosure duties remain: Written property disclosures listing all known defects are required in most states, regardless of what the contract says.

This last point trips up more sellers than anything else. Some people hear "as-is" and think they can stay quiet about a leaking roof or a cracked foundation. They cannot. Concealing known material defects exposes you to fraud claims that can survive closing. An as-is clause limits your repair and warranty obligations but never eliminates your duty to disclose what you know.

Pro Tip: Before listing, write down every issue you are aware of, from the HVAC that runs loud to the basement that floods in heavy rain. Your written disclosure protects you legally and sets accurate buyer expectations up front.

One more nuance worth understanding: financing type affects as-is deals in ways sellers rarely anticipate. FHA, VA, and USDA loans come with minimum property standards, and lenders may require repairs before they will fund the loan. A buyer with conventional financing or, better yet, cash avoids that problem entirely.

Repair vs. equity: when skipping repairs actually makes financial sense

This is where most distressed sellers make their worst mistake. They assume that fixing the house before selling will always yield a better return. The math often says otherwise.

Skipping repairs can be the smarter financial move when repair costs exceed the value those repairs add to the sale price. Consider a bathroom remodel that costs $18,000 but only adds $11,000 in perceived market value. You just spent $7,000 to net less. Add agent commissions and carrying costs during the renovation period, and the gap widens further.

Here is a practical comparison to frame your decision:

| Scenario | Cost | Impact on net proceeds |

|---|---|---|

| Full repairs before listing | $15,000 to $40,000 | May increase price, but rarely dollar for dollar |

| As-is sale with MLS listing | $0 in repairs | Lower list price, slower buyer pool, some negotiation expected |

| As-is sale to cash buyer | $0 in repairs | Below market price, but fast close, no commissions, no contingencies |

| Partial repairs (cosmetic only) | $2,000 to $5,000 | Improves presentation without major investment |

The financial case for selling in current condition gets stronger when you factor in what repairs actually cost in time. If you are facing foreclosure and your auction date is 90 days out, a kitchen renovation you thought would take three weeks often runs six. That delay has real consequences.

Pro Tip: Get three contractor quotes for any repair you are considering, then compare the total to what a local real estate agent estimates the repair will add in sale price. If the math does not clearly favor fixing it, skip it.

Deal-breaker issues are a separate category. Structural failures, active roof leaks, or electrical hazards that cause a property to fail basic habitability standards can make financing impossible for most buyers. For those specific problems, a cash buyer or a buyer using a renovation loan is often your only realistic path forward.

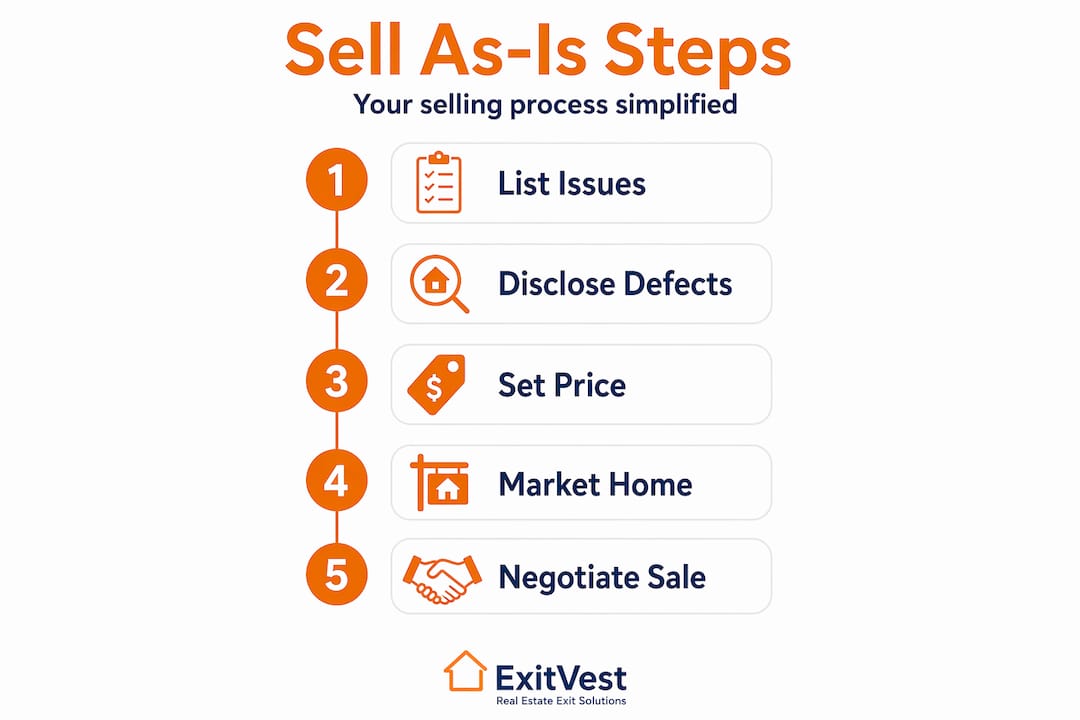

How to prepare and market your home when selling without fixing

Selling as-is does not mean throwing your listing up with blurry photos and hoping for the best. Preparation and positioning still matter. The difference is that your effort goes into presentation and honesty rather than repairs.

Here are the most effective steps for marketing a no repair home sale:

- State it clearly in the listing: Your agent's MLS remarks should explicitly say "sold as-is, no repairs, no credits." This filters out buyers who will waste your time demanding fixes.

- Price based on actual condition: Pull recent comps from your local MLS, then apply a condition adjustment downward. Overpricing an as-is home kills your momentum and stacks up days on market.

- Disclose everything in writing: Radical transparency shifts the legal burden to the buyer after disclosure and protects you from post-closing fraud claims.

- Target cash buyers and investors: These buyers expect distressed properties, move faster, and do not require lender appraisals that might flag repair conditions.

- Clean and declutter at minimum: You are not renovating, but a clean property photographs better, shows better, and signals that the condition issues are known and managed rather than hidden.

Transparency builds buyer trust faster than any upgrade. A buyer who discovers a problem after an accepted offer feels deceived. A buyer who sees it in the listing disclosure feels informed. That difference is what separates a smooth closing from a blown deal.

Navigating inspection contingencies and buyer negotiations

Even in a clearly disclosed as-is sale, the buyer's inspection period is where deals most often go sideways. Understanding the process in advance lets you stay in control without making concessions you cannot afford.

Here is how the inspection process typically unfolds in a property sold without fixing:

- Buyer orders inspection after accepted offer. This is standard in nearly all purchase contracts, including as-is deals.

- Inspector identifies conditions and writes a report. The buyer reviews findings and decides how to proceed.

- Buyer submits a request or response. In an as-is deal, they might ask for a price reduction, a modest closing cost credit, or simply accept the condition and move forward.

- Seller responds. You are not obligated to agree to anything. Citing the as-is price already accounts for condition is a legitimate and common response.

- Buyer decides to proceed or cancel. Inspection contingencies allow buyers to walk away if findings are unacceptable, even in as-is transactions.

- Deal closes or restarts. If the buyer walks, your disclosed listing record shows clean transparency, which helps with the next offer.

The smartest approach when a buyer pushes back is to offer a small, flat closing cost credit rather than a price reduction or actual repair. A $1,500 credit keeps a $180,000 deal alive. It is cheaper than relisting and faster than fixing anything. Just make sure any credit offered aligns with your lender's guidelines if you carry a mortgage.

Lead paint rules and lender repair requirements you cannot ignore

Two specific issues catch financially distressed sellers completely off guard, sometimes days before closing. Both deserve serious attention before you sign anything.

Federal lead-based paint disclosure rules apply to every home built before 1978, without exception:

- Sellers must provide buyers with an EPA-approved pamphlet on lead hazards before the sale.

- You must disclose any known lead-based paint or related hazards in writing.

- Buyers get a 10-day window to conduct a lead inspection unless they waive it in writing.

- Waiving that inspection period carries real risk. Lead remediation after closing can cost thousands, and a buyer who later discovers undisclosed lead hazards has a federal case against you.

For pre-1978 homes, these are not optional disclosures. They apply even when you are selling as-is, even when the buyer is an investor, and even when everyone involved agrees to skip formalities.

Lender-required repairs are the second trap. As noted earlier, FHA and similar loan programs will not close until required repairs are completed and re-inspected. If your buyer is using one of these programs, your as-is contract does not override the lender's appraisal requirements. The purchase agreement terms determine who pays for lender-required repairs, but the repairs still have to happen or the loan dies.

The practical solution is straightforward: target buyers who do not need lender approval. Cash buyers, hard money borrowers, and renovation loan buyers operate outside standard minimum property standard requirements. If you are under financial pressure and need a fast, certain close, those are the buyers worth pursuing.

My honest take on selling as-is during financial distress

I have seen sellers in real financial trouble spend their last $12,000 on a kitchen they could not afford because they were convinced the upgraded appliances would fix their situation. Sometimes the kitchen helped. More often, the money was gone, the house sat longer than expected, and they ended up back where they started but broker.

The conventional wisdom says fix it up to get the best price. My experience says that logic breaks down under financial pressure. When you are behind on payments, every week you spend renovating is a week of missed mortgage payments, accruing fees, and mounting stress. The goal stops being "maximize sale price" and becomes "maximize what you actually walk away with after all costs."

What I have found is that sellers who go the as-is route successfully share three habits. They disclose everything without embarrassment. They price honestly from day one instead of testing the market high and chasing it down. And they stop trying to attract the widest possible buyer pool and focus on the buyers who will actually close. That usually means cash buyers or investors.

The emotional shift matters too. Accepting that you will sell below market value is not failure. It is a calculated trade of price for certainty, speed, and freedom. That trade has real value when the alternative is foreclosure, carrying costs, or a renovation project that spirals past your budget.

— Alek

How Exitvest makes selling as-is simpler

If you are reading this because you need to sell quickly and cannot afford to fix anything, Exitvest was built for exactly your situation.

Exitvest buys homes as-is, nationwide, with a focus on New Jersey, Texas, Florida, and Tennessee. There are no repair demands, no listing delays, and no guesswork about whether a buyer's loan will fall through at the last minute. You request a cash offer, Exitvest evaluates your property, and you get a straightforward number with a flexible closing timeline that fits your situation. Whether you are facing foreclosure, an inherited home you cannot maintain, or simply a property draining your finances, you can see how the process works and take the next step without any pressure.

If foreclosure is the specific issue, Exitvest also has a dedicated path to help you stop foreclosure before it damages your credit further.

FAQ

What does selling a home as-is mean legally?

Selling as-is means you will not make repairs or offer repair credits, but you still must disclose all known material defects in writing. The as-is clause removes your repair obligation but does not eliminate disclosure duties under state or federal law.

Can I sell my house without repairs even if it has major problems?

Yes, you can sell a house without repairs even with significant issues, including structural damage or code violations. Your best buyer in that scenario is a cash buyer or investor, since lender-financed buyers may be blocked by minimum property standards on certain loan programs.

Do buyers still get an inspection in a no repair home sale?

Buyers retain their inspection rights in an as-is sale. They can inspect the home and use findings to negotiate or cancel during the contingency period, though you are not obligated to repair anything or reduce the price as a result.

How much less should I expect to get selling in current condition?

The discount varies by market and condition severity, but as-is sales to retail buyers typically run 10 to 20 percent below a fully repaired comparable. Sales to cash investors may go lower, but those deals close faster with fewer contingencies and no repair costs eating into your proceeds.

Does the lead-based paint disclosure rule apply to as-is sales?

Yes, federal law requires sellers of homes built before 1978 to provide an EPA-approved pamphlet and disclose known lead hazards before closing, regardless of whether the sale is as-is. Skipping this step creates significant legal exposure even after the deal closes.